Most people apply for a personal loan to fulfil their essential life goals. EMI (Equated Monthly Instalments) is one part of the equally divided monthly payment made to clear off an outstanding loan within a stipulated time frame. EMIs form a part of the repayment of personal loan that has been availed; this is a fixed amount paid by the borrower on a specified date every month. This EMI consists of two components:

- The principal amount

- The interest rate.

The principal is paid against the personal loan amount that one has availed while the interest is paid as a cost of providing the loan. This interest is either charged on the entire loan amount for all EMIs or on the reduced or outstanding principal amount left to be paid. Initially, the interest component constitutes the central portion of the payment. As you advance through the loan tenure, the part of interest repayment reduces and the contribution towards the principal repayment increases.

Factors Affecting Personal Loan EMI

The personal loan EMI depends on three key factors:

1) Personal Loan Amount: The total amount that has been borrowed by an individual.

2) Personal Loan Interest rate: The interest rate charged on the amount borrowed.

3) Personal Loan Tenure: The agreed-upon the loan repayment time-frame between the borrower and the lender.

How is EMI calculated?

There are two methods with which an EMI can be calculated. They are as follows:

1. Flat rate method:

Under this method, the interest rate is levied on the total loan amount regardless of the paid principal amount.

E.g. Ravi avails a loan of Rs. 1 Lakh at an interest rate of 8% p.a to be paid back in 3 years. As per this flat rate method, Ravi will pay the interest charged on the loan amount of Rs 1 Lakh.

The formula for the flat rate method to calculate EMI:

EMI = (Principal + Interest)/Period in Months

Interest rate for ! year= 8/100 x 100000= 8000

Interest rate for 3 years n =8000×3=24000

EMI = (100000 + 2400)/36 = Rs 3444.44

2. Reducing Balance Interest Method:

As per reducing personal loan EMI calculator, the interest is levied on the outstanding balance of the loan amount after repaying a certain amount of principal every month. The EMIs remain the same; however, the interest component in the EMI keeps reducing every month. When the personal loan amount of paid interest increases with longer terms, the loan EMI decreases if the loan is repaid over a more extended period.

The formula for reducing balance method:

EMI =

P x {[R x (1+R)^N] /[(1+R)^N-1]}

P = Principal Loan Amount = 100000

R = monthly rate of interest.

If the rate of interest per annum is 8%, then the interest is (8/12)/100= 0.0067 per month.

N = Monthly duration of the loan or the number of instalments = 36

So, as per the reducing balance method, the calculation would be:

EMI = 100000 x {[ 0.0067 x (1 + 0.0067)^36] / [(1+0.0067)^36-1]}= 3,135

If you go through both the methods, you will be able to understand that the EMIs calculated under the reducing balance method are generally lower than the flat rate interest method. The interest component in the reducing balance method would keep reducing every month, thereby saving on interest payments. The reducing balance method is the most commonly used method for calculating EMIs.

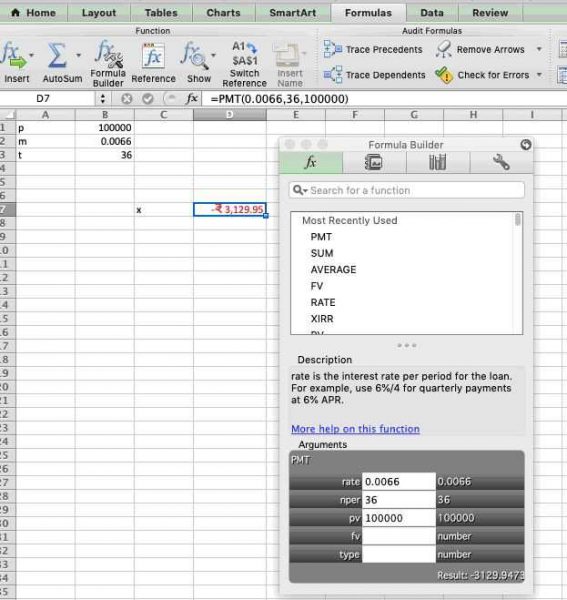

Calculating EMI Using Excel Spreadsheet

Use the MS-Excel formula “PMT” to calculate your loan EMI using an Excel sheet. The complete formula syntax for EMI calculation for Excel is:

PMT (rate, nper, pv)

Where,

rate = Personal loan interest rate (in percentage)

nper = Loan tenure in months, i.e. number of EMIs payable

pv = Loan principal (present value)

While the EMI calculation results will be the same whether you use the online personal loan EMI calculator or the Excel formula, the benefit of using the Excel formula is that you can use it offline as well.

Let us check the EMI for Ravi by using the PMT formula.

The rate used should be the monthly interest rate, that is, 8%/12= 0.0066

The number of periods represents the EMIs throughout the tenure.

=PMT(0.0066, 36, 100000)= 3,129.94

Bhupendra Singh Chundawat is a seasoned technology journalist with over 22 years of experience in the media industry. He specializes in covering the global technology landscape, with a deep focus on manufacturing trends and the geopolitical impact on tech companies. Currently serving as the Editor at Udaipur Kiran, his insights are shaped by decades of hands-on reporting and editorial leadership in the fast-evolving world of technology.